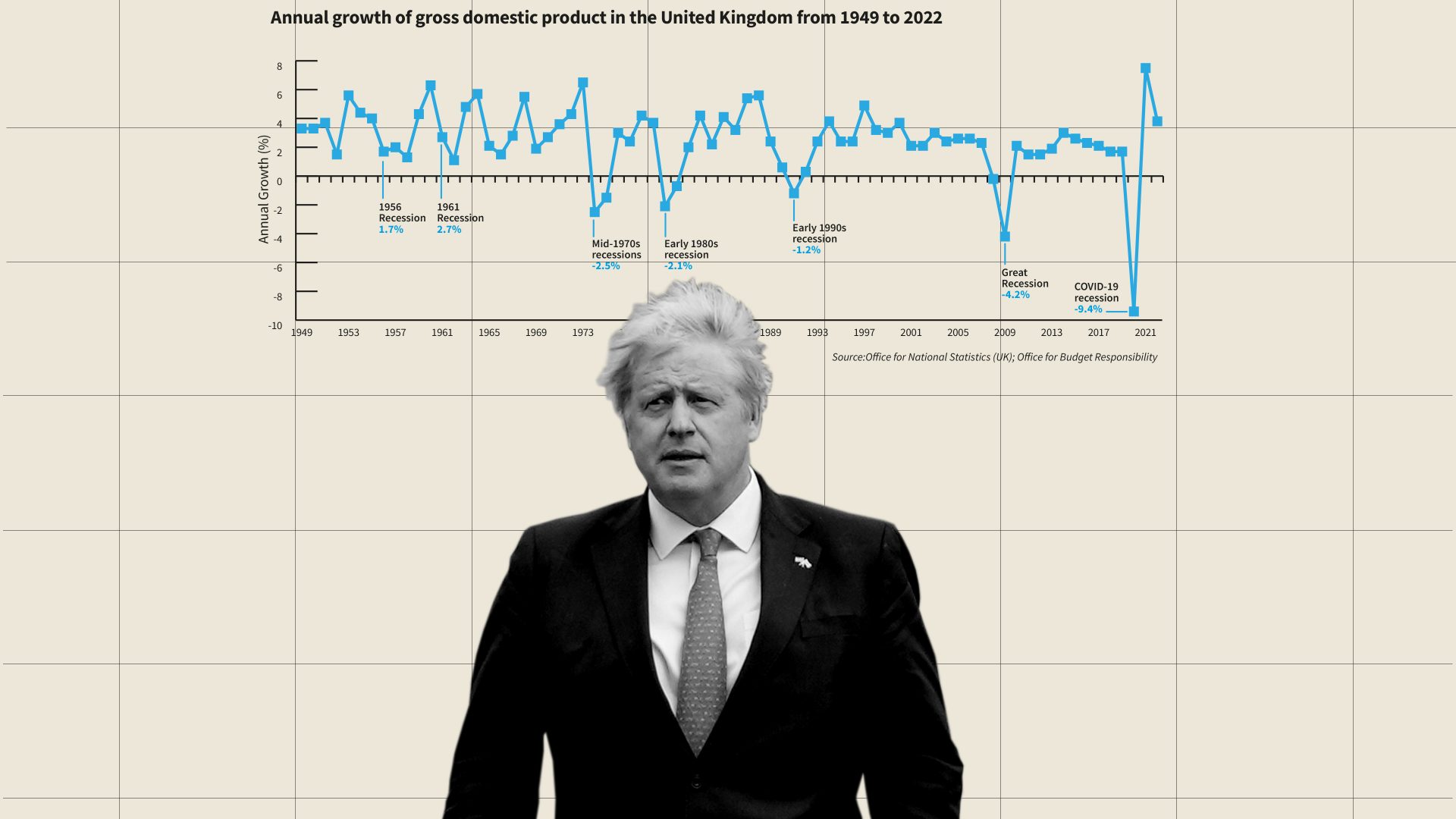

Recessions, at least in the UK, are defined as two consecutive quarters of negative growth. That is, six months when the economy contracts rather than expands. But it is not so much an economist’s definition of a recession as a politician’s.

My old boss Peter Jay used to point out where this definition came from. Apparently, US president Richard Nixon – on top of all his other problems – had to deal with a sharp economic downtown but managed to avoid calling it a recession by redefining it as a downturn that had to last over two consecutive quarters. It was, in fact, a bit of Tricky Dicky’s notorious, totally unprincipled, sleight of hand, political chicanery.

But the idea stuck, especially in the UK, and it now looks very likely the British economy will enter a recession. Certainly, the Bank of England is expecting one by the end of the year.

Recessions are a regular feature of any economy. We know they are out there somewhere, but not exactly when they will arrive or what will cause them. We can do little, or nothing, to stop them happening, but with the right policies we can weaken their effects and make them shorter and shallower than they might otherwise be.

Or, you can do nothing to prepare for them, make it easier for them to happen and make them much more painful and damaging than necessary when they do arrive.

Guess which camp the UK is in at the moment?

Although virtually no one saw the huge spikes in international energy prices coming, and even fewer expected the Russian invasion of Ukraine, they have happened. The consequences are already dire and are likely to get worse.

But the UK finds itself uniquely vulnerable to this latest downturn and the reasons why are easy to see.

Since the credit crunch in 2009, the British economy has been shuffling and stumbling along, with an uncertain gait, propped up only by the crutch of quantitative easing, which has meant throwing billions of pounds of free money at the economy every year – £450bn alone between 2020 and 2021. Despite that free money we have barely made it above a snail’s pace.

The figures don’t lie. In the 10 years before the credit crunch, the British economy grew by an average of 2.9% a year – a healthy rate of sustained growth. In the nine years between the end of the credit crunch and the arrival of Covid, the British economy grew by an average of 1.8%.

Why did growth collapse by 1.1 percentage points a year, or more than a third, immediately after the credit crunch and why did it stay so low? What happened to the UK’s long-term growth rate?

In short, it was wrecked by three factors. First, the near-collapse of the British and western world’s banking and finance sectors meant that there was permanent damage to the UK’s economy. Despite the Bank of England pumping billions a year into the system by printing money, the willingness and ability to spend and invest just wasn’t rebuilt. That meant disastrous levels of productivity, lower investment by British industry and less inward investment by foreign firms. All meant lower growth.

Second, the Cameron/Osborne government reacted to the biggest slowdown since records began by introducing austerity, slashing spending on welfare payments, housing subsidies and social services by £30bn and trying to balance the books.

Just when we might finally have been able to pick up the pace a bit, along came Brexit, which chopped the legs out from under the economy and from which it is unlikely to recover any time soon.

To put it in context, Brexit will destroy about 6% of economic growth in the UK. Considering that the average recession costs 2% and even that is soon regained by higher growth, this is the equivalent of three serious recessions from which we will never recover.

It is, therefore, not hard to see why the coming recession is going to hit the UK harder than most. All three factors mean the UK’s economy is easier to push into recession than those of its counterparts.

Before the credit crunch the British economy managed to grow on average by almost 3% a year; it took a lot of headwind to slow it down enough to create a recession.

After the credit crunch, British growth averaged 1.8%. This seems to be the permanent new “best” growth rate the economy can now sustain. It therefore takes less of a shock to slow it down enough to enter a recession.

Then Brexit takes another 6% off growth. Spread over 10 years, that is another 0.6% off annual average growth. That means it is now a good year when the British economy grows much above 1%. It is pretty easy to push such an economy into recession.

Brexit also means the safety valve of free movement of people has been destroyed. When times were good, East Europeans came to the UK to take up all those jobs we didn’t want to do. When the economy contracted they went home.

The absence of foreign workers leaves the Bank of England struggling with UK wage inflation and a recession at the same time. It has an overheated labour market and has to use high interest rates to cool it down, but it knows higher interest rates make recessions more likely, not less.

By comparison, Covid – economically speaking – was easy. It was a huge hit but a temporary and, hopefully, one-off hit. People and firms were paid to stay at home and the economy bounced back when it was allowed to reopen.

But while lower average annual growth means it takes a smaller shock to push you into recession, that just increases your vulnerability to future recession. The UK has a unique double whammy because it also has a government that is ideologically driven and therefore economically illiterate enough to think that cutting spending and using that money to cut taxes is the answer to any and all economic problems.

If the answer to every economic problem is to cut taxes and slash government spending, it is amazing that university economics departments and government finance ministries have anything to do all day. The answer is simple and universal, always slash spending and always spend the money on tax cuts instead. Hey presto!

Except that we know what is at the root cause of this recession. It is people not spending enough. You can see it on the petrol forecourt every day in the UK. As people spend more and more on filling their fuel tanks, they have less and less to spend on everything else, so they stop spending. They eat out less, buy fewer clothes, cars and TVs, they cut back on holidays and treats, all because the cost of energy has ripped money from their wallets and bank accounts.

If the government also slashes its spending, by building fewer schools and roads, cutting civil servants’ jobs, eviscerating departmental budgets and delaying pothole repairs, it too is ripping money out of the economy. Making the recession worse.

Cutting taxes helps, but not if you fund it by cutting spending. The net effect is zero or even negative, because in a recession when people get a bit more money they are always tempted to save it, in case things get worse, rather than spend it immediately. You have to borrow the money and use it to stimulate spending and, therefore, demand.

But this government is hidebound by its own ideology, it believes all government departments are vast money pits that can easily afford huge cuts to their budget without affecting their performance. Does anyone really believe 12 years after it first started its austerity programme that there is still enough money to be saved by “efficiencies” to pay for tax cuts from “savings”? Really?

This is obviously not based on reality but on an economic fantasy and the damage it will do will be massive. Just as consumer and business spending is tanking, government departments are going to cut their spending as well. A vicious circle of less and less spending and, therefore, less demand, all makes it likely we will suffer a deeper and deeper recession.

Just look at the dire performance of the economy after the credit crunch. George Osborne tried austerity and it failed. We have increased our susceptibility to a recession by lowering our long-term growth rate. And we are about to make the recession worse by an austerity policy that has already failed once.

If he survives that long, maybe Boris Johnson can escape the consequences of this crisis by just redefining the meaning of recession like Nixon did and calling it something else. But in the end, unprincipled chicanery didn’t do Tricky Dicky much good.